The Loan Life Cycle in the Subprime Short-Term Loan Industry

Date published: 08 APR 2025

Table of Contents

Introduction

The subprime short-term loan industry serves as a critical lifeline for millions who need quick access to cash but struggle to qualify for traditional loans. Whether it’s a payday loan to cover an emergency expense or an auto title loan to bridge a financial gap, these products help borrowers navigate challenging situations. However, issuing these loans, from application to repayment, is far from simple. Lenders must balance speed, risk, and compliance while ensuring fair treatment for vulnerable borrowers.

In this blog, we’ll walk through the complete loan life cycle, covering each stage from application to repayment or charge-off.

Also Read: How SparkLMS Empowers Lenders To Comply with the Small Dollar Lending Rule [SDLR]

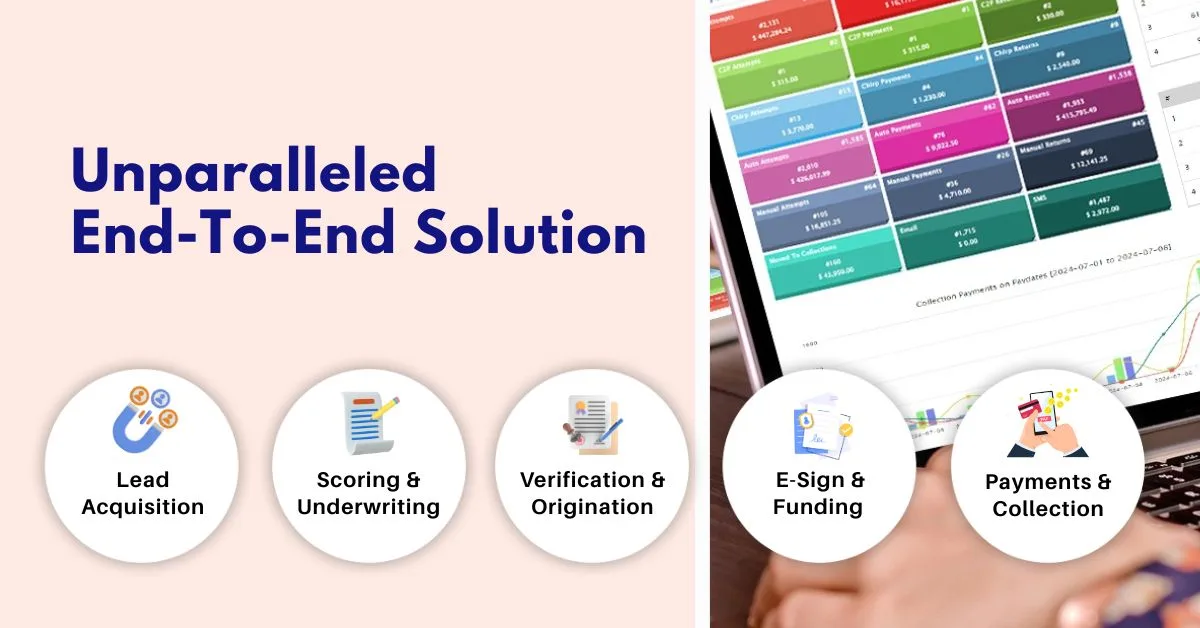

Loan Life Cycle: Subprime Short-term Loans

A subprime short-term loan life cycle begins with loan origination, followed by risk assessment, loan disbursement, repayment management, delinquency handling, and ultimately, loan closure. Each stage is crucial in ensuring responsible lending, minimizing risk, and maintaining compliance.

Loan Origination: Application & Borrower Assessment

The journey of loan life cycle begins when a borrower applies for a loan online, via a mobile app, or in person. At this stage, borrowers need clear explanations of interest rates, fees, and repayment terms without hidden surprises.

- Data Collection: The borrower's personal details, employment status, income sources, and bank account are verified.

- KYC & AML Compliance Checks: Lenders must comply with Know Your Customer (KYC) and Anti-Money Laundering (AML) regulations by screening against sanction lists and ensuring fund legitimacy to prevent fraud.

- Automated Screening: Tools like pre-qualification forms filter out ineligible applicants upfront, saving time for both borrowers and lenders.

- Loan Selection & Consent: Borrowers select the loan amount and repayment terms, while lenders disclose rates, fees, and conditions.

Comprehensive Risk Assessment

Subprime borrowers often have low credit scores or limited credit histories. To assess risk accurately, lenders need to look beyond traditional metrics.

- Credit Bureau & Alternative Data Analysis: Reports from agencies like Experian, Equifax, and TransUnion, along with non-traditional data sources (e.g., rent payments, utility bills, and telecom records), provide a holistic view of the borrower's financial behavior.

- Bank Account & Cash Flow Insights: Open Banking integrations (e.g., DecisionLogic, Plaid) assess payroll deposits, spending habits, overdraft frequency, and recurring expenses to determine financial stability.

- Fraud Detection & Identity Verification: Advanced fraud models identify suspicious activity, preventing synthetic identity fraud and loan stacking.

- Employment & Income Verification: Payroll data from sources like The Work Number or gig economy earnings confirm stable income, reducing default risks.

Loan Underwriting & Decisioning

After assessing risk, lenders determine loan approval, amount, and structure:

- Debt-to-Income (DTI) Ratio & Repayment Capacity: Ensures the borrower can afford repayment based on income, existing debt, and financial patterns.

- Automated Decisioning: Automated underwriting models streamline approval timelines and optimize risk-based pricing.

- Regulatory Compliance Checks: Validate that all loan terms align with federal and state lending regulations before final approval.

Loan Agreement & Fund Disbursement

Once approved, borrowers sign the loan agreement digitally or in person. The agreement includes:

- Loan Amount, Interest Rate, Fees, and Repayment Schedule

- Default, Late Fee, and Renewal Policies

- Mandatory Compliance Disclosures

Lenders then disburse funds via:

- ACH Bank Transfers: Bank transfers are secure and widely used for loan disbursement and repayments. Top processors include Repay, LoanPaymentPro, and Payliance.

- Instant Debit Card Disbursements: Enable faster funding through push-to-card services.

- Check Issuance: A traditional method for borrowers without direct deposit access.

- Cash Disbursement: Available at storefront locations.

- Digital Wallet Transfers: Emerging methods like PayPal, Venmo, or Cash App provide instant funding options.

Loan Servicing & Repayment Management

Once disbursed, the loan enters the servicing phase, where lenders ensure smooth repayment collection and borrower support:

- Automated Payment Processing: ACH debits, debit card payments, and mobile payment integrations minimize delays.

- Proactive Borrower Engagement: SMS, email, and phone reminders reduce missed payments.

- Flexible Repayment Options: Some lenders allow early payments, extensions, or installment modifications for borrowers facing financial hardship.

- Real-Time Risk Monitoring: Advanced analytics track borrower behavior, detecting early signs of repayment struggles.

Delinquency & Collections Process

If a borrower misses payments, the loan enters delinquency management:

- Grace Periods & Late Fees: Some lenders offer brief grace periods before imposing penalties.

- Soft Collection Strategies: Early-stage outreach through SMS, email, and customer service calls.

- Escalated Collections: If non-payment continues, cases may be handed over to collection agencies or legal recovery teams.

- Loan Charge-Off & Debt Sales: After prolonged delinquency, the loan is classified as a charge-off, and lenders may sell the debt to third-party agencies.

- Credit Score Implications: Borrowers are informed of potential credit score damage, encouraging resolution before further action is taken.

Loan Closure & Regulatory Reporting

If a loan is repaid or remains unpaid despite collection efforts, it enters the closure phase, requiring accurate reporting and compliance.

- Final Loan Settlement: The loan is marked as paid, written off, or refinanced based on the borrower's circumstances.

- Regulatory Reporting: Lenders update credit bureaus and maintain transaction records for audits.

Final Thoughts

Managing subprime loans requires automation-driven efficiency to reduce manual effort, ensure compliance, and enhance the borrower experience. With SparkLMS automated underwriting and real-time risk monitoring, lenders can make smarter decisions while maintaining regulatory integrity.

SparkLMS loan management platform simplifies the loan lifecycle with seamless automation and compliance support. Request a demo at [email protected].